Just an addition: if it is a rehearsal it could be for clearing the skies for air / missle defense since things are heating up war-wise with all the increased amounts of military equipment going against Russia. Possibly preparing for if and when the SHTF.This was posted on SOTT and it might be a rehearsal of some sorts as part of the Great Reset (or it could be EMF disturbances due to celestial events, or just a glitch for that matter).

View attachment 69218

The flights have since resumed after the disruption.

US Flights Disrupted - SOTT article

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

The Great Reset

- Thread starter Tolosa

- Start date

YES!!!

January 11, 2023

Oxford residents are taking matters into their own hands and destroying the street zone sectioning barriers.

Just recently there was a day of action by activists to kick start the year of fighting back. We predicted the UK was just getting started with their resistance, and here we have it. Taking matters into their own hands, Oxford residents are destroying street zoning barriers.

Piers Corbyn and friends are taking to the streets on Friday the 13th of January., Starting at Southwark tube in London.

thegreatclimatecon.com

thegreatclimatecon.com

OXFORD RESIDENTS MOUNT RESISTANCE AGAINST THE SECTIONING OF THEIR STREETS

15 Minute Cities, On The GroundJanuary 11, 2023

Oxford residents are taking matters into their own hands and destroying the street zone sectioning barriers.

Just recently there was a day of action by activists to kick start the year of fighting back. We predicted the UK was just getting started with their resistance, and here we have it. Taking matters into their own hands, Oxford residents are destroying street zoning barriers.

Further action

There are further planned dates for activists to take to the streets in various forms of protest.Piers Corbyn and friends are taking to the streets on Friday the 13th of January., Starting at Southwark tube in London.

Oxford Residents Mount Resistance Against The Sectioning Of Their Streets - The Great Climate Con

Oxford is quickly becoming the centre of the fightback against The Climate Con. Citizens of the UK are taking matters into their own hands.

FWIW, article from Infowars;

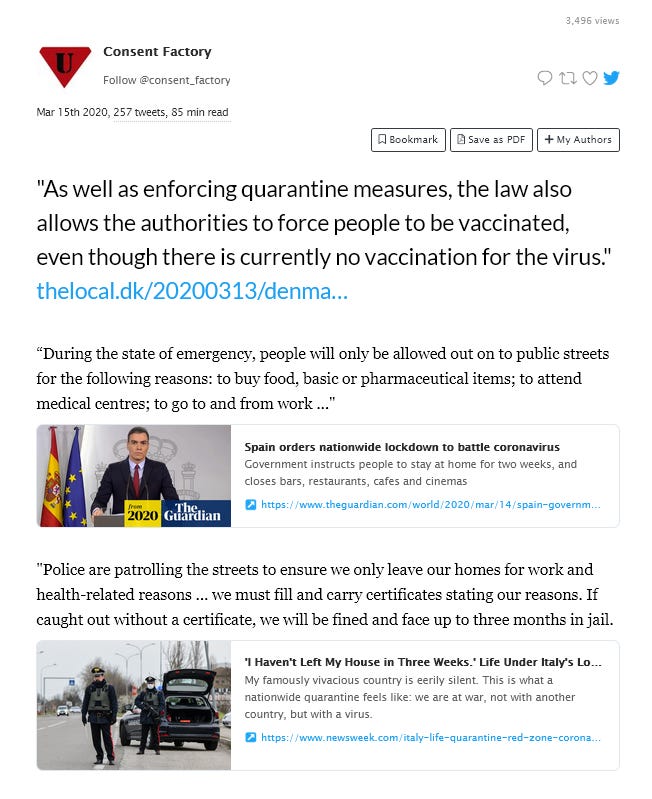

Must Watch: FDIC Bankers Discuss ‘Bail-Ins’ To Deal With Impending Market Collapse

November 2022 meeting shows financial regulators plot how to hide alarming market signals from depositors to prevent a bank-run panic.

www.newswars.com

Magnolia

Jedi

Have only listened to 1/3 of the video, but if you can get through the acronyms and euphemisms, it seems the 'next crisis won't be 2008" and runs on banks are a concern to them. It's getting late, but it's interesting enough to pursue the rest tomorrow.

They talk about Title I and II. Seems that, according to FDIC website:

Section 165(d) of Title I of Dodd-Frank Act: The DFA requires the FDIC and the Federal Reserve Board to review resolution plans submitted under Section 165(d), and we may jointly make a determination of whether a plan is not credible or would not facilitate an orderly resolution of the firm under the U.S. Bankruptcy Code. Each resolution plan, commonly known as a “living will”, submitted under Section 165(d) must describe the firm’s strategy for rapid and orderly resolution under the U.S. Bankruptcy Code in the event of material financial distress or failure of the company. These living wills must include both confidential and public sections.

Under Title II of the Dodd-Frank Act, bankruptcy is the first [and primary] resolution option in the event of a failure of a systemic financial company. To make this prospect achievable, Title I of the act requires that all large, systemic financial companies submit living wills to demonstrate how they would be resolved under the bankruptcy code. This will enable both the firms and regulators to understand and rationalize the parts of a SIFI’s business that are not suited for bankruptcy and take the necessary steps to address impediments. The objective is to have a credible plan demonstrating how resolution under the bankruptcy code would be orderly and not pose systemic risks.

Resolution Strategy - Key Objectives

Stability

Minimize financial instability in the US financial system

Consider direct and indirect effects

Market and public confidence

Accountability

Ensure the failed company’s investors bear the losses arising

from failure

No potential of taxpayer credit support

Potential assessment to the industry to cover “overpayments”

Statutory requirement not to retain culpable management

Viability

Successor firm(s) operate with no government support

Market confidence established

Expedient process for re-privatization

Avoid increasing market concentrations

They talk about Title I and II. Seems that, according to FDIC website:

Section 165(d) of Title I of Dodd-Frank Act: The DFA requires the FDIC and the Federal Reserve Board to review resolution plans submitted under Section 165(d), and we may jointly make a determination of whether a plan is not credible or would not facilitate an orderly resolution of the firm under the U.S. Bankruptcy Code. Each resolution plan, commonly known as a “living will”, submitted under Section 165(d) must describe the firm’s strategy for rapid and orderly resolution under the U.S. Bankruptcy Code in the event of material financial distress or failure of the company. These living wills must include both confidential and public sections.

Under Title II of the Dodd-Frank Act, bankruptcy is the first [and primary] resolution option in the event of a failure of a systemic financial company. To make this prospect achievable, Title I of the act requires that all large, systemic financial companies submit living wills to demonstrate how they would be resolved under the bankruptcy code. This will enable both the firms and regulators to understand and rationalize the parts of a SIFI’s business that are not suited for bankruptcy and take the necessary steps to address impediments. The objective is to have a credible plan demonstrating how resolution under the bankruptcy code would be orderly and not pose systemic risks.

Resolution Strategy - Key Objectives

Stability

Minimize financial instability in the US financial system

Consider direct and indirect effects

Market and public confidence

Accountability

Ensure the failed company’s investors bear the losses arising

from failure

No potential of taxpayer credit support

Potential assessment to the industry to cover “overpayments”

Statutory requirement not to retain culpable management

Viability

Successor firm(s) operate with no government support

Market confidence established

Expedient process for re-privatization

Avoid increasing market concentrations

Last edited:

Swiss Army Sends 5000+ Soldiers to Guard Davos Globalist Elites

"Some 5,000-plus soldiers from the Swiss army are deployed to welcome attendees to the luxury ski resort and protect participants from any harassment, protests or dissenting voices.""As Breitbart News reported, this year’s meeting is headlined “Cooperation in a Fragmented World” and will follow on from the Great Reset as declared at the Davos summit of 2021."

"Forum president Borge Brende said some delegations had asked for the names of their participants “not to be shared” right away for security reasons, adding unspecified “high-level” delegations from China and Ukraine would attend but no further details will be released."

"The U.S. will be represented by Biden administration officials including presidential climate envoy John Kerry, head of national intelligence Avril Haines and U.S. Trade Representative Katherine Tai as well as several governors and congressional lawmakers."

Swiss Army Mobilises Up To 5000 Soldiers to Guard Davos Globalist Elites

The Swiss army has up to 5,000 soldiers mobilised to protect the globalist elites attending the World Economic Forum annual meeting.

www.breitbart.com

www.breitbart.com

XPan

The Living Force

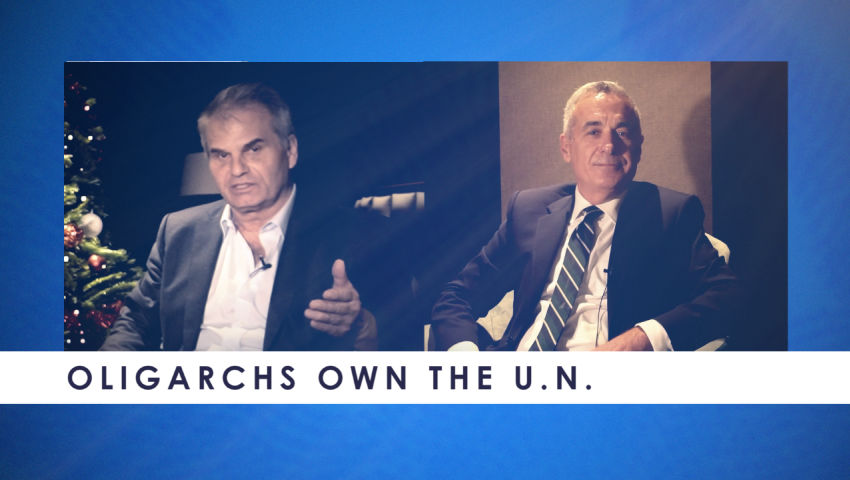

ICIC • "Oligarchs own the UN"

English • 1h 4 min

video.icic-net.com

video.icic-net.com

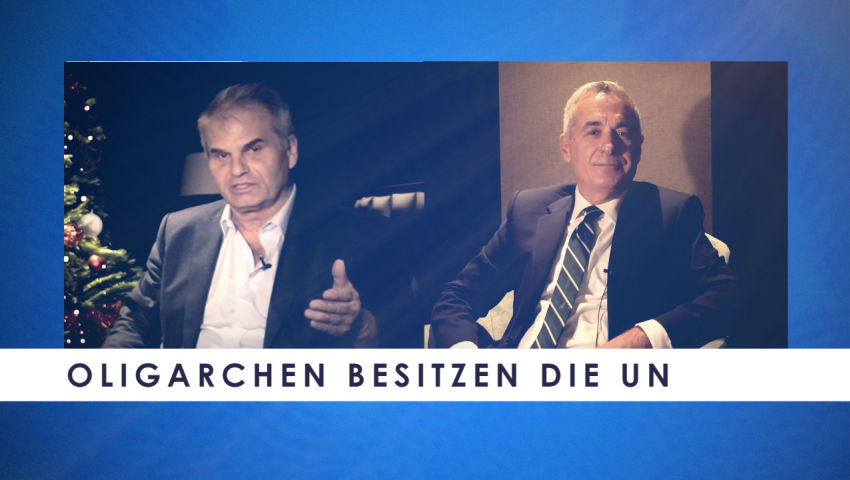

English with German subtitles • 1h 4 min

video.icic-net.com

video.icic-net.com

This video interview with former UN Executive Director Călin Georgescu impressed and surprized me a lot. It is the kind of interview which grows along the session, crystalizing out a man with stamina, knowledge of how the system is underpinning humanity via the NGO's such as UN and WEF. He also seems to be a man of faith; What resides in the core in humanity's spirit. What really matters - and what does not.

However, the interview is mainly about how the system works, behind the scenes, in the corridors of the UN and the "WTF" (WEF) (Schwab's World Economic Forum) or Club of Rome. How intentionally good organizations turned twisted and corrupted over time.

English • 1h 4 min

Oligarchs own the U.N.

In this revealing and insightful interview. former UN Executive Director Călin Georgescu describes the process of infiltration and global takeover of the United Nations by oligarchs, particularly Klaus Schwab and the World Economic Forum (WEF). He outlines the power structures of the UN, its...

video.icic-net.com

English with German subtitles • 1h 4 min

Oligarchen besitzen die U.N.

Seien Sie dabei, wenn der ehemalige UN-Exekutivdirektor Călin Georgescu in diesem aufschlussreichen Interview den Prozess der Unterwanderung und der globalen Übernahme der Vereinten Nationen durch Oligarchen, insbesondere Klaus Schwab und das Weltwirtschaftsforum (WEF), beschreibt. Er skizziert...

video.icic-net.com

This video interview with former UN Executive Director Călin Georgescu impressed and surprized me a lot. It is the kind of interview which grows along the session, crystalizing out a man with stamina, knowledge of how the system is underpinning humanity via the NGO's such as UN and WEF. He also seems to be a man of faith; What resides in the core in humanity's spirit. What really matters - and what does not.

However, the interview is mainly about how the system works, behind the scenes, in the corridors of the UN and the "WTF" (WEF) (Schwab's World Economic Forum) or Club of Rome. How intentionally good organizations turned twisted and corrupted over time.

In this revealing and insightful interview. former UN Executive Director Călin Georgescu describes the process of infiltration and global takeover of the United Nations by oligarchs, particularly Klaus Schwab and the World Economic Forum (WEF).

Hi_Henry

The Living Force

Yes, coal is dirty.

However it stops being dirty when "The Owners" are effected in the pockets.

www.zerohedge.com

www.zerohedge.com

The joke is on the people in whose countries coal mines are being closed, resulting in electricity bills climbing like a helium balloon. Not to mention small/medium businesses closing.

But hey, "We must do our part to help !!!"

However it stops being dirty when "The Owners" are effected in the pockets.

A Big Green Mess In Germany With Coal A Stunning 31% Of Electricity Production | ZeroHedge

ZeroHedge - On a long enough timeline, the survival rate for everyone drops to zero

www.zerohedge.com

The joke is on the people in whose countries coal mines are being closed, resulting in electricity bills climbing like a helium balloon. Not to mention small/medium businesses closing.

But hey, "We must do our part to help !!!"

That was a great interview!! So good to see a soul who has seen into the heart of the Beast on some level at higher levels and is willing to speak out with such clarity and strength. A thought provoking interview to share with others who are awakening and seeking an overview of the Agenda that is not filled with doom, gloom and fear, instead reality and positive potential. Thankyou XPan!This video interview with former UN Executive Director Călin Georgescu impressed and surprized me a lot. It is the kind of interview which grows along the session, crystalizing out a man with stamina, knowledge of how the system is underpinning humanity via the NGO's such as UN and WEF. He also seems to be a man of faith; What resides in the core in humanity's spirit. What really matters - and what does not.

However, the interview is mainly about how the system works, behind the scenes, in the corridors of the UN and the "WTF" (WEF) (Schwab's World Economic Forum) or Club of Rome. How intentionally good organizations turned twisted and corrupted over time.

Emerald Rob

Jedi Council Member

A Prison Where The Prisoners Don't Know They're In Prison

Emerald Rob

Jedi Council Member

How to opt out of a technocratic state

Tess Talks with Derrick Broze

How to opt out of a technocratic state

Watch now (58 min) | Tess Talks with Derrick Broze

drtesslawrie.substack.com

drtesslawrie.substack.com

Magnolia

Jedi

FDIC officials discuss how to deal with approaching market collapse and prevent bank runsFWIW, article from Infowars;

Thank you for making us aware of this information. I watched the video on the webpage. It was long and strenuous.

I am giving 'my take' on what I heard in the video because information is suppressed; the public is being kept in the dark.

I think it is important to stay tuned so as not to be immobilized when things happens.

This post has three parts.

1) Some information I gathered from the video.

2) Some acronyms with short explanations.

3) Information from Investopedia which is a "Cliff Notes" explanation of the Dodd Frank machinations they have imposed on us.

If the first 2 parts are dull, skip to the 3rd for the 'powerpoint' explanation.

Part One

My Opinion: Bank and global financial system failures seem to be one of Main Agenda items, on the same "short list" as destruction by fabricated wars, death by the medical consortium, and control by famine.

It seems that our beloved concept of FDIC insurance is passe, the Dodd-Frank Act has taken over (created via the 2008 problem/reaction/solution process), the crash will be global ("cross-border"), the first bank default(s) will occur on a weekend, there will be runs on banks, the crash will entail a whole cascade of events, it will be a shock to the system, and FDIC and Big Gov't will come in and 'save us' by using our personal savings and retirement funds to bail out institutions that they consider "too big to fail." "Too big to fail" seems to mean any money-laundering ponzi organization that the PTB need in order to continue their machinations and preserve their quality of life. The small banks don't matter -- small depositors can take them over by getting (possibly worthless) bank shares in lieu of their hard-earned money. In the process, the citizen covers all the costs, pays all the prices, and becomes the pauper. But The Regime marches on -- maintaining, or improving, its status quo.

Video Summary

Disclaimer: When it comes to Dodd Frank financial matters, I have no idea what I am talking about. The Dodd Frank Act is (deliberately, I figure) complex and convoluted. So, this is just my limited and uneducated interpretation of what I heard on the video. There is better information on the web and FDIC website.

Since the video is available to the public, the participants mince words, over-use acronyms, repeat euphemisms, and engage in a lot of deliberate word salad splattered with pseudo-language which clearly indicates they are either really stupid or have something to hide. They are clearly not stupid (in one sense, anyway).

For example, one person literally states, "A huge challenge is what to do with a bank which has a balance sheet where there's equity and deposits and nothing in between." Say what? You have to interpret or read between the lines to figure out what they are talking about. To me, "equity + deposits and nothing in between" COULD mean a successful -- vs failing -- bank. But they won't come right out and say that. Oddly, this kind of bank really worries them. They ask: How do we handle such situations? Can we impose the financial burden of large bankrupt institutions on such a bank?

Some Key Points from the Video

- There seem to be two main points of systemic failure: large banks and large non-bank central clearinghouses (CCP).

[In the U.S., a CCP is called a derivatives clearing organization (DCO) which is regulated by CFTC-Commodity Futures Trading Commission. They are concerned about the level, or lack, of coordination between FDIC & CFTC when failures occur. Other countries don't seem to have the same problem.] - The goal of this video group, and the goal of the resolution (failure) rules, and everything enacted into law is designed to "protect adverse effects on US financial stability" (2:23). Apparently "US Financial Stability" does NOT take into account the well being of its citizens. Regarding proper interpretation of their use of the term financial stability, and the function of the Organization of Financial Stability, reference SOTT article The aristocracy is eating the peasants

- Many terms are unknown to me and had to be searched (e.g., bail-ins, bridges, haircutting [reduce your bank deposits by x%], waterfalls, Quantum, clearinghouses, "resolutions" [a euphemism they cling to like a life preserver, meaning financial institute failures]). Not once did I hear the word "depositor" or "deposits," despite the fact that it is our money they intend to steal, "legally," to cover their ponzi tactics.

- At some point, a lengthy posting of all their acronyms and terminology, with explanations, could provide a lot of clues to their strategy and tactics.

- The key players in this global financial manuever are Bank of England, Fed, SEC, CFTC-Commodity Futures Trading Commission (US agency overseeing derivatives, futures, swaps, options) & FDIC.

- There are quotes in the video re timing. Bank failures are apparently planned for a weekend: "The message that we will send out on Friday night." They state, "There is a decision making authority about when and which weekend institutions fail on so we hope we will not be resolving multiple institutions at the same time." (1:54)

- They claim to not know what exactly will happen or when, but they expect "it" to happen very quickly with little or no warning.

- They use phrases like “WHEN [not if] the time comes."

- They state "Large banks will almost certainly fail due to a run on liquidity," "40-50% of depositor accounts are uninsured," How saleable are these [financial] institutions under resolution? There will be a very limited set of possible acquirers. The firms might have to be broken into 'buckets' to sell them. We may have to do bail-ins and have investors take them over.

- They continue to say they may have to escalate from Title I to Title II (but this is obviously the plan).

- They talk loosely that losses will be allocated (but they never specifically divulge how they are allocated). There are many euphemistic statements like "compensation claims are subordinated to general creditors and prior compensation can even be clawed back" -- which means what? but nonetheless this seems like a horrific red flag for depositors.

- As they focus on protecting government/corporate/PTB wealth by using citizen funds, one person states Maybe we need to consider what to do about Joe's Auto Shop which will need funds to pay its employees each week. The reaction was silence, so it seems (a) a lot more work must be done before things actually start to happen, or (b) there's lots of room for total chaos when they start.

- There was talk of "transparency." Summarized comments are, I think you would scare the public. They would ask why are you telling me this. There could be unintended consequences of blasting this out to the public. They have more faith in the banking system than people in this room do." One woman wants more information to be available to the public, "but not the whole hog." They want transparency "that will lend stability in a negative outcome."

- They are very concerned about the appearance (versus the reality) of transparency and want to ensure general public audience confidence in the process and the FDIC. One fellow suggests that transparency would be more effective if it were "accurate." (ha! good for him). They intend to publicly fire a bunch of "culpable" managers -- probably so the public can blame someone and be satiated with some lynchings. Dream on.

- They are quite concerned about non-bank financial institutions. The timing of CCP clearinghouse failures is less controllable; they can't plan for it to occur on a weekend. Prices will move rapidly in the market, and things could get out of control, but they hope their stepping in will inject "stability."

- According to Sir Jon Cunliffe, Deputy Governor for Financial Stability Bank of England: If non-CCP institutions fail, the CCP will have an imbalance on its spreadsheets -- they'll suffer a loss in relation to their collateral and there will be rapid effects. CCPs could 1) absorb losses (but they have no capital, so that doesn't work). 2) Pass their losses without limits back to their clearing members using established loss allocation rules. 3) Use the pre-funded default fund. 4) When the default fund is depleted (which will occur quickly), the CCP makes cash calls (possibly multiple cash calls) on the remaining members. 5) Then they "haircut"/vary margins to members. 6) They tear up some or all of the contracts they have. 7) Since they can't go bankrupt; they just disappear.

- Cunliffe states, "The equity of the owners is untouched in that process." [Really? Who are these owners? I couldn't find them.]

- NDL Non Default CCP losses are clearinghouse losses related to operations/business/legal risks, cyber risk, & fraud. "This is a really big problem," they state. NDLs cannot be allocated to members. The "general audience public" can't bail them out. Most of the default rulebook cannot apply. This group is not authorized to take the actions they'd like to, and it could lead to almost immediate failure of the clearinghouse. BOE wants to ensure that "Resolution Authorities" are involved quickly in NDLs so they can act outside the rulebook to protect special interests. Measures are proposed in Parliament now to ensure they get these "extra powers" [including intervention, decision-making and rule-making]. Cunliffe also suggests they should increase the default fund since a) owners have no "skin in the game;" b) members might refuse cash calls -- although that would immediately put them in default; and c) issuing bonds to cover losses could have some serious consequences.

Part Two: Summary of Some Definitions Use in the Video

Dodd-Frank Act /Authority allows the FDIC to resolve a large bank holding company or a systemically important non-bank financial institution when its default would have serious adverse effects on the financial stability of the United States.

"We do not have the framework, infrastructure, authority in place on the non-banking side [i.e., CCP] that we have on the banking side." But: "They are going to happen at the same time."

Title I gives line of sight into the companies' financial status, and authority to get them to make changes and design plans to facilitate bankruptcies.

Title II gives authority to supervise default processes for banks and global systemic banking organizations in order to inflict an orderly and fast liquidation fund backstop (i.e., no bail-out).

TLAC (Total Loss-Absorbing Capacity) is an international standard, finalised by the Financial Stability Board (FSB) in November 2015, intended to ensure that global systemically important banks (G-Sibs) have enough equity and bail-in debt to pass losses to investors and minimise the risk of a government bailout. (TLAC rules were changed in 2020 which appear to increase the chances for bank failures.)

FSOC Financial stability oversight council: #2 To promote market discipline by eliminating expectations on the part of shareholders, creditors, and counterparties of such companies that the U.S. government will shield them from losses in the event of failure.

CCP Central counterparty clearing houses emerged from the 2008 crisis as lynchpins of the global derivatives markets........By standing in the middle of a trade, the CCP assumes the credit risk of each side of the trade [buyer and seller]. When a member defaults because of extreme (not “normal”) market conditions, then contributions and resources of all members would be called upon to support the CCP if the defaulting member’s own collateral and contributions together were insufficient. The video noted that, since 2008, 60% of credit derivatives now go through CCP. Before only 10% did. Today 85% of interest rate contracts go through CCP. Before only 40% did.

CCPs now play a huge role in commodity markets, particularly hedging and forward contracts.

Regarding Sir John Cunliffe/BOE He says, "The Committee on Payments and Market Infrastructures (CPMI) deals with life; the Resolution Authority deals with death...." Ultimately, "ll costs are passed back to users. There is no way users can avoid the costs.

Cunliffe's video section starts at 2:32:17 to the end. He speaks comparatively clearly if anyone is interested in watching just a portion of the film.

When searching information on-line, it became clear that

Not everyone is keen on Dodd-Frank. For example:

2014: "Dodd-Frank has drawn fire as encouraging, rather than preventing, bailouts. Detractors urge repealing Title II of Dodd-Frank and amending the Bankruptcy Code to include a new Chapter 14 in its place.....with it's starkly contrasting aims of reorganizing troubled companies, preserving going concerns and maximizing payments to creditors."

2018: The Trump Administration and Republicans have initiated efforts to repeal certain provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank), one of which is the Orderly Liquidation Authority (OLA) under Title II of Dodd-Frank.

2014: FDIC Coverage And Dodd Frank – What It Could Mean For Your Deposits:

---OLA "Orderly Liquidation Authority" receivership rules state that the Federal Reserve and FDIC now have the authority, under financial distress, to convert your cash deposits, savings, and CD's at the bank into equity shares of the bank itself in order to make the bank whole. This is often called a "bail-in."

---OLA permits the FDIC to repay the banks obligations to its depositors with stock instead of cash. OLA permits conversion of the banks obligations to its depositors, ie savings accounts, checking accounts, CD's, to stock.

Part Three: INFORMATION FROM INVESTOPEDIA

Investopedia (and many other sites) has some human-language clarifications and suggestions, summarized below:

- Big banks got government (taxpayer) bailouts in 2007-2008.

- Financial reforms ushered in with the Dodd-Frank Act eliminated bailouts and opened the door for bail-ins.

- Rather than bail out banks, the federal government shifted the risks to creditors by allowing financial institutions the ability to use debt capital to keep themselves afloat. This means that debtholders, unsecured creditors, shareholders, and depositors can be responsible for problems within the financial sector.

- Bail-ins allow banks to convert debt into equity to increase their capital requirements.

[One person in the video defined "bail-in" as turning the bank over to its creditors. 2:06] - They shift the risk to unsecured creditors, including depositors whose account balances exceed the FDIC limit of $250,000. [Whether this $250k insurance coverage will hold, I cannot discover. There are internet comments that contest that the $250k will be convertible to cash, on-call. There are also internet comments which hypothesize that if you have $260k in one bank the entire amount will be subject to the bail-in. It is not clear to me, and probably isn't meant to be.]

Bail-ins and bailouts are designed to prevent the complete collapse of a failing bank. With bailouts, the government injects capital into banks, enabling them to continue their operations. During the financial crisis, the government injected $700 billion of taxpayer funds into Bank of America, Citigroup, AIG, and others.

Under bail-ins, banks use money from their unsecured creditors, including depositors and bondholders, to restructure their capital to stay afloat. Put simply, they can convert their debt into equity to increase their capital requirements. Although depositors run the risk of losing some of their deposits, banks can supposedly only use deposits in excess of the $250,000 protection provided by the Federal Deposit Insurance Corporation (FDIC).

Unsecured creditors, depositors, and bondholders fall below derivative claims. Derivatives are investments that banks make among each other, which are supposed to be used to hedge their portfolios. However, the 25 largest banks hold more than $247 trillion in derivatives, which poses a tremendous amount of risk to the financial system. To avoid a potential calamity, the Dodd-Frank Act gives preference to derivative claims.

Bail-Ins Become Statutory

The provision for bank bail-ins in the Dodd-Frank Act was largely mirrored after the cross-border [global] framework and requirements set forth in Basel III International Reforms 2 for the banking system of the European Union. It creates statutory bail-ins, giving the Federal Reserve, the FDIC, and the Securities and Exchange Commission (SEC) the authority to place bank holding companies and large non-bank holding companies in receivership under federal control.

Europe Experiments With Bail-Ins

One of the key examples of the use of bail-ins was in Cyprus, a country saddled with high debt and the potential for bank failures. The country's banking industry grew at an alarming rate after Cyprus joined the European Union (EU) and the Eurozone. This growth, coupled with risky investments in the Greek market and risky loans from two large domestic lenders, led to the need for government intervention in 2013. A bailout wasn't possible.......Instead, it instituted the bail-in policy, forcing depositors with more than 100,000 euros to write off a portion of their holdings—a levy of 47.5%.

.....These bail-ins may become more widespread. Investors are concerned that the increased risk to bondholders will drive yields higher and discourage bank deposits. With the banking systems in many European countries distressed by low or negative interest rates, more bank bail-ins are a strong possibility.

In 2013, the EU introduced resolutions to make the bail-in a common principle by 2016 in response to the effects of the European Sovereign Debt Crisis. It transferred the responsibility of a failing banking system from taxpayers to unsecured creditors and bondholders, the same way Dodd-Frank did in the United States.

How to Protect Your Assets (according to Investopedia)

Bail-ins are the new norm. Banks have the authority to take control of any capital that fits the criteria as per the law. This means anyone who has an account that exceeds the $250,000 insured limit may be affected. Anything above that amount can be used for bail-in purposes. If you want to protect your assets, here are a few tips you may want to take into account:

- Keep a watchful eye on the performance of the financial markets and financial sector

- Ensure the financial institutions you choose are financially secure and stable

- Spread the risk by diversifying your money and assets across different banks and countries

- Keep balances at or below the $250,000 limit

- Make sure you monitor any changes to federal government policies about bank deposits

- Don't bank with any institution that has large derivative and mortgage books, which can be risky in times of crisis

To quote Cass: Fear Not. Knowledge Protects, Ignorance Endangers.

And as one author notes, "It is very easy to be desperate; life offers us these opportunities every step of the way. For some people, it is good to be desperate all the time. It results in ceaseless prayer, and ceaseless prayer will get you enlightened—you will see the light."

Last edited:

Mods, can you merge the following threads with this one and make the title "The Great Reset"???

cassiopaea.org

cassiopaea.org

Ports of Unrest - Navigating Full Spectrum Dominance and the Great Reset

This thread is for monitoring ongoing shenanigans at various ports around the world in the Great Reset era. There are cross-over threads, but this one is meant to just track the events taking place at ports and supply chains affected by unrest in any form. After the Beruit bombing last year...

cassiopaea.org

If you don't read anything else of this article, read the part I've put in bold.

The Mother of All Limited Hangouts

CJ Hopkins

Jan 11

The Mother of All Limited Hangouts has begun. Yes, I’m talking about the “Covid Twitter Files,” which are finally being released to the public, in almost textbook limited-hangout fashion. I’ll get into that in just a minute, but first, let’s review what a “limited hangout” is, for those who are not familiar with the term.

The way a limited hangout works is, if you’re an intelligence agency, or a global corporation, or a government, or a non-governmental organization, and you have been doing things you need to hide from the public, and those things are starting to come to light such that you can’t just deny that you are doing them anymore, what you do is, you release a limited part of the story (i.e., the story of whatever it is you’re doing) to distract people’s attention from the rest of the story. The part you release is the “limited hangout.” It’s not a lie. It’s just not the whole story. You “hang it out” so that it will become the whole story, and thus stop people from pursuing the whole story.

Victor Marchetti, a former special assistant to the Deputy Director of the CIA who went on to become a critic of the Intelligence Community, described the tactic this way in 1978 …

“… a favorite and frequently used gimmick of clandestine professionals. When their veil of secrecy is shredded and they can no longer rely on a phony cover story to misinform the public, they resort to admitting, sometimes even volunteering, some of the truth while still managing to withhold the key and damaging facts in the case. The public, however, is usually so intrigued by the new information that it never thinks to pursue the matter further.”

All right, so, you’re probably asking, if the “Covid Twitter Files” are a limited hangout, what’s the whole story that they’re distracting us from?

Let me try to refresh your memory.

In March and April of 2020, in the course of roughly five to six weeks, the majority of societies throughout the world were transformed into pathologized-totalitarian police states. A global “shock-and-awe” campaign was conducted. Constitutional rights were suspended. The masses were locked down inside their homes, where they were subjected to the most massive official propaganda blitzkrieg in human history. Goon squads roamed the streets of Europe, the USA, the UK, Canada, Australia, Asia, the Americas, and elsewhere, beating and arresting people for being outdoors without permission and not wearing medical-looking masks. Corporate media around the world informed us that life as we knew it was over … a “new normal” was coming, and we needed to get used to it.

The entire official pandemic narrative was rolled out during those first few weeks. Everything. Masks. Mandatory “vaccines.” “Vaccination” passports. The segregation of “the Unvaccinated.” The censorship and demonization of dissent. Everything. The whole “New Normal” package. It was rolled out all at once, globally.

If your memory of what happened is a little hazy … well, have a look at this 257-tweet Twitter thread of corporate-media articles compiled in March and April of 2020, documenting the initial “shock-and-awe” campaign …

That is the story. How that happened. Why that happened. And who or what made it happen. It isn’t a story about a virus, or our governments’ reactions to a virus. It is the story of the radical restructuring of society based on lies and official propaganda, executed, globally, through sheer brute force and systematic psychological conditioning. It is the story of the implementation of our new totalitarian global-capitalist “reality” … the “New Normal” that was announced in the Spring of 2020. It is not a story the global-capitalist ruling classes can permit to be told, except by “crazy conspiracy theorists,” “science deniers,” and other “crackpots” and “extremists.”

All right, so … the “Covid Twitter Files,” or the “Fauci Files,” or whatever we’re calling them. If you wanted to bury the actual story (i.e., the story I just outlined above) with a limited hangout and discredit those of us who have been trying to report it for nearly three years, you couldn’t do any better than Elon Musk is doing. Instead of a story about how the entire global-capitalist power apparatus coordinated with global IT corporations like Twitter, Facebook, Google, et al., to conduct a global Gleichschaltung op the scale of which Goebbels could have never dreamed of, censoring and visibility-filtering dissent and enforcing the official pandemic narrative, not just in the USA, but in countries all throughout the world … instead of that monumental story, we are getting The Alex Berenson Show!, starring Alex Berenson as Alex Berenson, with a special guest appearance by Alex Berenson, written and directed by Alex Berenson, and so on.

Seriously, though, who better to handle the “Covid Twitter Files” than Alex Berenson, in whose opinion the events of the last three years were simply due to mass hysteria (or Pandemia, $14.99 on Amazon), and certainly not to any kind of coordinated radical restructuring of society by the global-capitalist power apparatus, or any other wild conspiracy theories. Forget about that 257-tweet thread I compiled in March and April of 2020. What actually happened, according to Alex Berenson, was that people just went kind of crazy, and overreacted, and “mistakes were made.” Mistakes like Twitter suspending Alex Berenson, and other very important people! Or, wait, no, it wasn’t just mass hysteria … it was also Pfizer and Dr. Scott Gottlieb, and the White House, and someone named Andrew Slavitt, all of whom conspired with “Old Evil Twitter” to suspend Alex Berenson from the platform, all of whom Alex will be suing forthwith!

The Alex Berenson Show is just getting started, so definitely stay tuned to “Free-Speech Twitter” to follow all of Alex Berenson’s exploits as he leads “Team Reality” to its ultimate victory over “Team Apocalypse” and exposes the crimes of the usual assortment of official “bad apples,” or whatever cartoonish fairy tales Alex Berenson and Elon Musk have in store for us! It promises to be quite the spectacle!

I’ll be covering the show in my columns, of course — I still have a few subscribers and readers who I haven’t totally alienated yet — and discussing “The Art of the Limited Hangout” for the benefit of anyone still paying attention in the weeks and months and possibly years ahead. If you are one of the many people who now appear to seriously believe that military-contractor oligarchs like Elon Musk and narcissistic ass clowns like Alex Berenson are going to deliver us from the New Normal Reich, and “prosecute Fauci,” and end corporate censorship, or in any way meaningfully bite the hand of the global-capitalist system that feeds them, you may want to give those columns a miss.

For the rest of you, I will do my best to point out how this phase of the PSYOP works, because it’s going to last for quite a while. The “Covid Twitter Files” are not The Mother of All Limited Hangouts; they’re just one part of it. There are many more limited hangouts to come. The New Normal having been successfully implemented, the history of its implementation is now being written (or, rather, rewritten) to conform to the official Covid narrative, a process which will likely continue for years.

Those of you who are old enough might recall this phase from “The War on Terror.” It started around April 2004, when the Abu Ghraib torture photos were released, and continued until the Summer of 2016, when The War on Terror was abruptly cancelled and replaced by The War on Populism, which prepared us for the implementation of the New Normal in the Spring of 2020. All of which is part of an even larger story, i.e., the story of the evolution of the first globally-hegemonic power system in history, which, lacking any external adversary, has nothing to do but go totalitarian, eliminating all internal resistance and establishing ideological uniformity throughout the territory it occupies, which, in this case, means the entire planet.

Sorry … I know, history is boring, and complicated, and not nearly as fun (and cathartic) as the shit-slinging circus that Musk is making of the Twitter Files. Personally, I can’t wait to find out which official “bad apple” they’re going to offer us in today’s edition of the Two Minutes Hate, and who’s going to be released from “Old Twitter Prison,” and, whatever, anyway, don’t worry about all that evolution-of-global-capitalism stuff. It’s probably just a bunch of fancy-sounding nonsense I made up to try to sell you my books, or to make myself sound smart, or something.

Forget that I even mentioned that stuff. Sit back, relax, and enjoy the show!

Pat

Jedi Master

I understand Elon Musk as follow:

An hungry power individual getting comfortable with his accumulation of money and power will never ever release freely his power to help out little people without being compensated one way or the other. It's not in his/her set of mind to do things for free... we are giving him/her sentiments/quality they don't have.

An hungry power individual getting comfortable with his accumulation of money and power will never ever release freely his power to help out little people without being compensated one way or the other. It's not in his/her set of mind to do things for free... we are giving him/her sentiments/quality they don't have.